Wang’s Café Goes Green: Innovative Finance Solutions for Small Companies

Peter Knaack | 27 March 2025

Monetary, Blog | Tags: China, Entrepreneurship, Financial Inclusion, Green Finance

Wang, the owner of Wang’s Café, is taking serious steps to make his café greener. He wants to replace fluorescents with LED lights, install low-flow faucets, buy a high-efficiency oven, switch to paper bags, and start to compost food scraps. He heard the government supports environmental initiatives and offers a discount on the loan he will need to finance these investments. But the banks he approaches either offer no preferential loans for green investments, or if they do, they ask him whether each of his intended purchases fits the green taxonomy (they don’t). Some even want him to report his carbon footprint in tons of CO2 equivalent/year. An expensive endeavor. Getting a third-party agency to calculate his carbon emissions or certify his environmental performance costs around $10’000 a year. He can’t pay that much, and the bank won’t either. And that’s where the green finance journey of most small companies ends.

Green finance is not inclusive, and inclusive finance is not green. Financial markets have mobilized a large and growing amount of money for climate action – but most of it goes to large firms. Small companies (micro, small, and medium-sized enterprises or MSMEs in the jargon) account for around half of economic output and around half of greenhouse gas emissions around the world. But they struggle to access the finance needed to green their activities. A survey by the European Banking Authority (2023) finds that while green loans make up ca. 4.5% of European bank loan portfolios, that share drops to 2% for non-retail SMEs and close to zero for retail SMEs (see Figure 1).

Figure 1: Share of green loans in total loans (by business line), sample of 83 European financial institutions

Source: EBA (2023) Report on Green Loans and Mortgages

In a recent paper, we identify two main reasons why small companies struggle to access green finance:

- Current green finance standards and products (taxonomies, green loans, green bonds) are made for big firms and sovereigns – they rarely fit the business realities of small companies.

- Green due diligence, the process of assessing the environmental performance of a client, is expensive.

Unsatisfied with that situation, several green finance pilot cities in China’s Zhejiang Province and MYBank (an online bank headquartered in Zhejiang) have come up with innovative approaches to tackle this problem. Pilot cities in China are cities that are selected by the central government to develop experimental new policies, for example, in the field of green finance. MYBank has pioneered an in-house model that rates the environmental performance of small companies using simple, easy-to-collect data, such as the company’s electricity and water bills (see Figure 2).

Figure 2: MYBank’s Greenness Rating Model

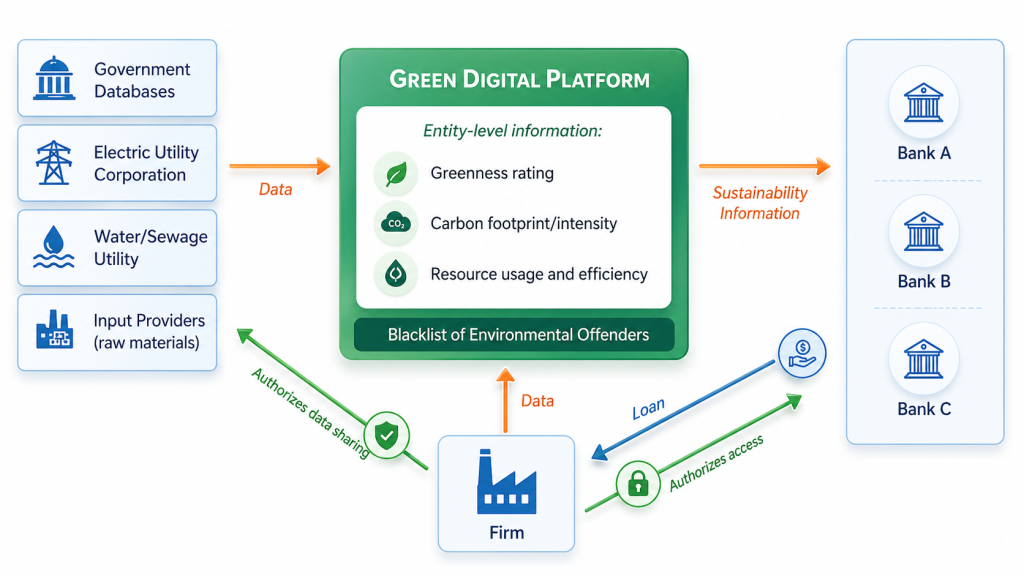

Zhejiang’s pilot cities have developed their own rating models. In addition, they established public green digital platforms that use firm-level information to calculate a carbon footprint and a greenness rating. They then make this information available to local banks, with the firm’s authorization (see Figure 3). This way, banks have access to green due diligence at little to no cost. And banks that offer loans to good environmental performers can count on policy support in the form of credit guarantees and interest rate subsidies from the municipal government. MYBank has discovered that the top green performers among its clients are also significantly less likely to default on their loans – an additional reason to treat them well.

Figure 3: Green Digital Platforms

This approach has had some effect: Since Zhejiang’s pilot cities established green digital platforms, the volume of green loans has risen significantly, especially for small companies. In Taizhou, the share of small companies in the green loan portfolio of local banks rose from 3.3% in June 2021 to 7.8% in October 2022. In Huzhou, it reached 8% by end-2024.

Green digital platforms have three advantages:

- They make green due diligence cheaper and easier. The setup of Zhejiang’s municipal platforms required an initial public investment of approximately 3 million yuan (ca. $410,000), with annual maintenance costs ranging from 15% to 30% of that amount, according to our interview partners. In their absence, each bank would have to spend about the same amount on a proprietary system. Green digital platforms also eliminate the need for third-party certifications for firms.

- They provide relatively reliable information. The risk of a borrower exaggerating improvements in their environmental performance (greenwashing risk) is reduced because some or all of the data comes from independent sources. It is not easy to cheat on your water bill to pretend you are greener than you are.

- They work almost everywhere. Data such as electricity use may only render a rough carbon footprint estimate, but it is a good first approximation, and it is widely available. Reports on green finance in emerging markets and developing countries often decry a lack of granular data as an obstacle. Maybe the obstacle is not a lack of data, but a lack of ingenuity?

But green digital platforms are not a panacea for inclusive green finance either. The information they provide is only useful if banks want to boost green lending, and if firms have a reason to invest in greening their activities. Providing policy incentives is not cheap. Some city governments allocate 10 billion yuan (ca. $1.4 billion) annually to fund interest subsidies for green loans, credit guarantees, and premiums for private credit default insurance. More research is needed to find out which incentive scheme provides the biggest bang for the buck.

Wang can make his café greener with the help of a loan that gets cheaper if he treats the environment better. Whether that happens or not depends on whether he can count on an adequate information environment and policy incentives for him and the bank. Zhejiang has some lessons to offer.

Read the full discussion note Inclusive Green Finance for Small Companies: A Case Study of Pilot Cities in China’s Zhejiang Province, by Jingyi Zhang, Peter Knaack and Danqing Shao.

Related Posts

Inclusive Green Finance for Small Companies: A Case Study of Pilot Cities in China’s Zhejiang Province

Jingyi Zhang, Peter Knaack and Danqing Shao | 21 February 2025Monetary, Discussion Notes | Tags: China, Entrepreneurship, Financial Inclusion, Green Finance

Micro, small, and medium-sized enterprises (MSMEs) are crucial for the transition to a sustainable economy. However, they face major challenges in accessing financing for sustainable investments.... continue reading

Inclusive Green Finance: a New Agenda for Central Banks and Financial Supervisors

Ulrich Volz and Peter Knaack | 23 June 2023Monetary, Policy Briefs | Tags: Financial Inclusion, Green Finance

Through an integrated inclusive green finance (IGF) approach, central banks and financial supervisors can enable a just transition to an environmentally sustainable economy and avoid potential adverse effects on economically... continue reading

Does Fintech Promote Entrepreneurship? Evidence from China

Peter Knaack | 24 January 2023Monetary, Blog | Tags: Digital Economy, Entrepreneurship, Fintech

Policy moves and public statements in recent years indicate that Beijing seeks to simultaneously support the growth of internet finance platforms and reign in anticompetitive practices and risky behavior.... continue reading

Greening Financial Governance: Lessons from China

Peter Knaack | 13 January 2022Monetary, Discussion Notes | Tags: China, Governing Finance, Green Finance, Macroprudential Policy

China’s turn towards green financial governance has causes and consequences that are instructive for policymakers elsewhere. This paper traces the evolution of rules and regulations designed to guide China’s financial... continue reading