How California Leaders Can Improve the Oversight and Evaluation of State Tax Expenditures

Kayla Kitson | 6 September 2024

Fiscal, Blog | Tags: Parliaments, Tax Expenditures, United States

This article is part of a blog series on the critical role of parliaments in tax expenditure policy making. The contributing authors include members of parliament, government officials, and further experts in the tax expenditure field. Additional blogs in the series are available on the Philippines, the Netherlands, the United States, and Zambia. The introduction to the series is available here.

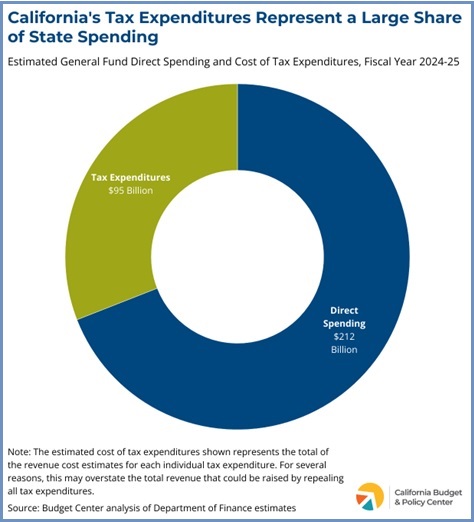

In California, tax expenditures — defined in state law as a “credit, deduction, exclusion, exemption, or any other tax benefit as provided for by the state” — represent a significant revenue cost to the state. In recent years, the estimated cost to the state’s General Fund of personal income tax, corporate tax, and sales tax expenditures has ranged from more than $80 billion to nearly $95 billion. As a point of reference, the enacted state budget for state fiscal year 2024-25 includes an estimated $212 billion in direct spending.

It should be noted that the cost estimates produced by state offices for some tax expenditures are very uncertain due a lack of precise data. In addition, due to the effects of interactions between tax expenditures and potential changes in taxpayer behavior that would result from the repeal of tax expenditures, totaling the estimated costs of each tax expenditure does not necessarily reflect the total revenue that would be gained from repealing all tax expenditures. However, this comparison provides some insight into the magnitude of revenue the state forgoes by keeping these tax expenditures in place.

Increasing the transparency, oversight, and evaluation of tax expenditures is a significant concern because although these expenditures take resources off the table that the state could be investing in other public services, they receive far less scrutiny than direct state spending. This means that tax expenditures often continue from year to year without discussion, even when there is little or no evidence that they are effective in achieving their intended goals. Moreover, many large tax expenditures disproportionately benefit higher-income individuals and highly profitable corporations.

State Tax Expenditure Reports

Currently, both the state’s Department of Finance (DOF) and the Franchise Tax Board (FTB) produce annual tax expenditure reports with estimates of the costs of each expenditure.

The FTB reports are not required by law, but have generally been released annually. Historically, the have contained detailed information, including a discussion of the policy rationale for each expenditure and factors that might determine whether the expenditure is effective in achieving its goals. Additionally, the FTB reports contain data on the distribution of tax benefits by income level when that information is available. The of the FTB report does not include the policy discussion for each tax expenditure, focusing only on the cost and distributional estimates. If this continues to be the case in future reports, policymakers, researchers, and advocates will have less transparent information to help them evaluate whether continuing a tax expenditure may be justified.

The DOF tax expenditure reports are required by state law (Government Code Section 13304). The DOF reports have not historically provided information on the distribution of tax benefits. However, a state law enacted last year added this requirement for tax expenditures where there is available data. Of course, there are many tax expenditures without distributional data, particularly those that provide exclusions or exemptions of items from taxable income, since these are generally not reported on tax forms. For example, some of the tax expenditures estimated to have large costs are related to the exclusion of the value of employer-provided non-cash benefits such as health insurance and contributions to retirement plans. In practice, these types of tax expenditures are likely to disproportionately benefit people in higher-earning jobs with more access to robust benefits, but we do not have data to examine the distribution of benefits.

Shortcomings of California’s Tax Expenditure Oversight Practices

While the state tax expenditure reports provide valuable information on the estimated cost and distribution of benefits, California has no regular, comprehensive process for reviewing and evaluating tax expenditures. Some tax expenditures have been analyzed by the state’s nonpartisan Legislative Analyst’s Office pursuant to statutory requirements or on an ad hoc basis — such as the film credit and the California Competes economic development credit — but the state has no broadly applicable policy for evaluating the impacts of tax expenditures. Additionally, there is no process for incorporating the findings and recommendations from these analyses into the policymaking process.

In 2016, the California State Auditor produced a report examining the cost effectiveness of select business tax expenditures, requested by the Joint Legislative Audit Committee. However, the Auditor noted that there was insufficient evidence to determine the effectiveness of two of the six expenditures they reviewed, including the Research and Development Credit — the state’s second-largest business tax expenditure. The Auditor noted that the lack of evidence with regard to these tax expenditures was due to the fact that no state entity regularly evaluates them. And while the State Auditor recommended that the Legislature adopt best practices for tax expenditure oversight used in other states — including clearly defining policy objectives and performance measures, establishing sunset dates and requiring regular evaluations, and connecting the evaluations to the policymaking process — this has not yet happened.

In a 2017 review of the practices of all 50 states and the District of Columbia, the Pew Charitable Trusts classified California as one of 23 states “trailing” in adopting best practices for evaluating tax expenditures. While this review focused primarily on economic development tax incentives, Pew found that many states identified as “leading” or “making progress” also included other types of tax expenditures — such as those benefiting individuals — in their tax expenditure evaluation laws. Since the 2017 report, additional states have made progress in adopting tax expenditure evaluation laws, but California continues to be in the minority of states without such a law.

California policymakers have taken some steps toward improving tax expenditure accountability by enacting legislation requiring that bills creating new tax expenditures include goals, detailed performance indicators, and data collection requirements. A 2014 law applied these requirements to new personal income and corporate income tax credits, and a 2019 law extended those requirements to all new personal and corporate income tax expenditures and sales tax exemptions. A recently enacted law exempted tax expenditures that are exclusions from income from these requirements if the Legislature determines there is no available data to collect, since information on items excluded from income is generally not reported on tax returns.

However, these laws do not apply to existing tax expenditures. This is problematic because the state’s most costly tax expenditures have been in effect prior to the enactment of these laws and are able to escape the additional scrutiny. Legislators can also avoid including goals, performance indicators, and data collection requirements in their tax expenditure proposals by simply stating in their bill language that those requirements do not apply.

Legislative committee chairs have the power to enforce these laws by mandating that tax expenditure bills adhere to the requirements in order to pass out of the committee. For example, the Chair of the Revenue and Taxation committee in the state Assembly has a policy that in order to be eligible for a committee vote, bills creating, extending or expanding a tax expenditure must comply with the requirements and must generally include a 5-year sunset date. However, any committee chair can choose whether to enforce the requirements.

Recent Attempts to Improve Tax Expenditure Oversight and Evaluation

In recent years, some state policymakers have attempted to create a more formal process for evaluating tax expenditures, but unfortunately those efforts have not succeeded. In 2019, a bill to create a one-time evaluation process for specific tax expenditures passed in the Legislature but was vetoed by Governor Newsom. The bill would have narrowly targeted large business tax expenditures that did not already have sunset dates or requirements to report efficacy metrics. The bill would have required an evaluation of the applicable tax expenditures by the University of California and created a California Tax Expenditure Review Board, which would have been required to review the evaluation and make recommendations to the Legislature based on the findings. Similar bills were introduced in 2020 and 2021, but both died in legislative committees.

Recommendations

California leaders can take several steps to increase the scrutiny given to tax expenditures with the goal of ensuring that 1) state resources are being used in a cost-effective manner, and 2) the state’s tax system helps to increase equity.

The Pew Charitable Trusts’ 2017 report identified key best practices for states in evaluating their economic development incentives, and I argue that these practices should apply to tax expenditures more generally. The recommendations include:

- Requiring a nonpartisan entity to regularly evaluate the effectiveness of tax expenditures and making sure the entity has access to the data needed for a robust analysis;

- Ensuring the evaluation analyzes the extent to which the tax expenditures influence behavior and considers the trade-offs the state is making by forgoing state revenue that could be spent on other public services;

- Requiring that the findings of evaluations be considered in legislative hearings where stakeholders can submit input; and

- Setting expiration dates to encourage policymakers to consider evaluation findings when deciding whether to renew, modify, or repeal tax expenditures.

These evaluations should also examine whether a given tax expenditure furthers economic and racial equity, or if it perpetuates or widens existing inequities. Policymakers should also consider the equity implications of tax expenditures in their decisions to create, extend, modify, or eliminate any tax expenditure.

Taking these steps toward greater scrutiny of California’s tax expenditures will ensure that policymakers and members of the public are more informed when making or advocating for state budget decisions that have meaningful impacts on people’s lives. A better understanding of the equity impacts and cost effectiveness of these costly but opaque types of state spending will put state leaders and advocates in a better position to work toward a California where everyone is able to prosper.

Related Posts

Advancing Scrutiny: 55 Year of Tax Expenditures Reporting in the United States

Jane G. Gravelle | 14 December 2023Fiscal, Blog | Tags: Parliaments, Tax Expenditures, United States

The normal baseline currently used to define tax expenditures by the US Treasury remains fairly close to an economic measure of income, but with some differences. Tax expenditures include employee... continue reading

Tax Expenditure Scrutiny Can End Trillion-Dollar Political Game

Flurim Aliu, Doug Koplow and Agustin Redonda | 19 January 2023Fiscal, Commentary | Tags: Income Tax, Inequality, Tax Expenditures, United States

Too often, government spending is understood only as cash payments to specific individuals or groups. However, targeted exemptions or reductions in taxes owed strain public coffers similarly to direct spending,... continue reading

Reforming Tax Expenditures – Challenges and Barriers in the United States

14 April, 2021 20.00 CET, 14.00 EDT | OnlineFiscal, Panel | Tags: Tax Expenditures, Tax Reform

The panel addressed the main challenges and barriers holding back reform of the tax expenditure system in the US including: The politics of tax expenditures “Negative” and “positive” tax expenditures Collecting racial, ethnic,... continue reading