How Much Revenue Does Kosovo Forgo Through Tax Expenditures? We don’t know!

Flurim Aliu | 21 April 2022

Fiscal, Blog | Tags: Tax Expenditures, Transparency

This article was originally published in Albanian by sbunker here.

The traditional way of thinking about how states finance projects is as follows: first, governments collect revenue (through taxes, borrowing, payments, and fines) and then this revenue is spent through the budget process.

However, governments may choose to support various economic sectors, activities, or groups of taxpayers through preferential tax treatment, e.g., through exemptions, deductions, tax credits, reduced tax rates, and other forms of tax expenditures. Tax expenditures refer to potential revenue which the state forgoes to support different population groups or different economic sectors, which, in one way or another, constitute a form of expenditure.

However, unlike direct expenditures (salaries of public officials, financing of infrastructure projects, etc.), the use of tax expenditures is often hidden from the public eye. In general, most direct spending programs have to go through the budget process and are subject to yearly public scrutiny through parliamentary inquiries and media discussions. Tax expenditures, to the contrary, are often approved only once and then not debated again in the budget processes. In this way, the latter can lead to a misallocation of states’ financial resources.

How much revenue does Kosovo forgo through tax expenditures?

At a time when states are facing increased fiscal pressure to finance the fight against the COVID-19 pandemic and other problems such as the energy crisis and increasing prices, reforming or suspending some tax expenditures could provide the government with additional revenue to fulfill its duties.

However, the Government of Kosovo does not know how much revenue it forgoes through tax expenditures. In this way, Kosovo joins Belarus, Bosnia, Croatia, Montenegro, Moldova, and Serbia as the only countries in Europe that do not assess and report revenue forgone through tax expenditures.

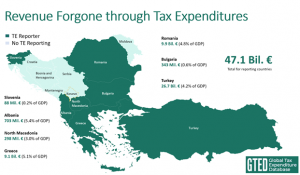

This, despite the fact that this forgone revenue can reach enormous figures. On average, about 4% of the gross domestic product (GDP) of different countries worldwide and 25% of their tax revenues are forgone as a result of tax expenditures for different groups of individuals or companies. The average is similar when looking only at Balkan countries (see the figure below).

In North Macedonia, the first tax expenditures report, published in 2021, revealed that tax expenditures cost the country about 300 million Euros a year (about 3.0% of GDP). In Albania, the latest detailed report of tax expenditures, also published in 2021, estimated that the Albanian state treasury forgoes over 700 million Euros per year as a result of tax expenditures (5.4% of GDP). In both countries, most of these expenditures came in the form of various VAT exemptions. In Albania, the VAT exemption for the public administration and VAT exemptions for the real estate sector, with about 100 million Euros each, were among the largest provisions.

Source: Author’s work, using data from www.GTED.net

If Kosovo is close to this average, it could be giving up between 200 and 300 million Euros in potential revenue per year. However, the exact figures can only be estimated by the Government of Kosovo, which so far has never assessed the revenue it forgoes by offering different tax incentives.

Why should the Government of Kosovo estimate its tax expenditures?

Estimating these costs is necessary for several reasons. First of all, while it can be said that some tax reliefs, such as the VAT exemption of food products in Albania, may be justifiable, some others, such as the VAT exemption of Albanian Parliament members (which cost state over 76 thousand Euros in 2015), are much harder to justify and may need to be removed or reformed.

Additionally, the estimation of tax expenditures, in addition to being potentially economically beneficial, is also important in Kosovo’s political process of European integration. The European Union (EU), the International Monetary Fund (IMF), and the World Bank have repeatedly called on Kosovo for increased transparency in tax spending. For example, the latest IMF Article IV Consultation report on Kosovo, published this year, called on the government to estimate and report its tax expenditures. Plus, through a directive approved in 2011, the European Commission requires all its member and candidate countries to start preparing detailed tax expenditure reports.

Therefore, the assessment, reporting, and finally, the reform of tax expenditures is a necessary step that the Kurti Government could use to increase Kosovo’s revenue.

To reform tax expenditures, the Ministry of Finance should take five concrete steps. First, it should review tax legislation to discover all the legal provisions that constitute tax expenditures. Second, it should estimate how much revenue the state forgoes through these tax breaks (using annual tax returns as well as other statistical methods). Third, it should assess what the objectives of each of these tax expenditures are. Fourth, it should evaluate whether these tax expenditures have achieved their set goals. And fifth and finally, it should reform or eliminate those tax expenditures that do not meet the intended goals.

Undertaking this process would clearly demonstrate that the current government is trying to deliver on its electoral promises of properly allocating state resources.